There is this blind faith that wherever Amazon comes, jobs will be created. It is not true. Studies have shown over and over again that there are no net gains in jobs, In fact, at year three in almost every single location, there is no net area job gain.

It disrupts the local employment market, by initially draining workers from surrounding minimum wage jobs now that that Amazon promotes the $15/hr rate, but it does not provide sustainable long term employment. They have on average a 90% attrition by the end of the first year. That is why every facility is continually hiring and requires no experience or background checks.

In the retail sector, from which most employees are draw the during the first year of operation, studies show that for every 2 jobs Amazon creates, the retail sector loses 3.

So the myth of job creation distorts the picture by encouraging support for an illusionary increase in jobs. And we must not forget that even at $15/ that is less than $30,000 gross a year. Who can reasonably raise a family on that income? That is why Amazon is now the largest company with the highest percentage of total employees on government assistance in the country.

At the same time, its corporate employees as a group are the best paid in North America. Even more than better known tech companies on average.

Below are articles related to employment for you read and verify the facts. You will also notice that the Amazon department responsible for monitoring any negative press will have contacted the media with “corrections” to blunt the negative aspects of what the reporter uncovered. Some media even acknowledge this in small print at the bottom of their articles. So when you an article was revised, it almost always was after Amazon stepped into to alter the content.

The sequence is just in the order by which I uncovered it by doing google searches. The most revealing was on pages 2 through 6 in the search of the results, so you may want to first read those at the bottom.

Everyone can form his own opinion after examining the facts, but simply repeating the myth that Amazon equals new jobs is just the ostrich with his head in the sand.

In addition, at the end is background on the robots, automation, and drone use at distribution centers.

Murray Bilby

Amazon’s anti-union PR efforts amid Alabama vote are a very bad look

No matter what happens in Bessemer, Jeff Bezos’ response shows exactly what workers are fighting for.

People protest in Los Angeles in support of unionizing efforts by Alabama Amazon workers on March 22.Lucy Nicholson / Reuters

April 1, 2021, 3:56 PM EDT

By Paris Marx, host of the “Tech Won’t Save Us” podcast

On Monday, the voting period for workers looking to form a union at the Amazon fulfillment center in Bessemer, Alabama, ended, and whatever the result, it’s clear that the company is feeling the pressure.

In the weeks leading up to the vote, the workers in Bessemer were showered with support from politicians like Stacey Abrams and Sen. Bernie Sanders, I-Vt., celebrities like Danny Glover, the Major League Baseball and NFL players’ unions, allies across labor both domestic and international and even President Joe Biden, who recorded a video denouncing anti-union propaganda.

As the union vote approached, Jeff Bezos became incensed by negative coverage, according to Recode.

The campaign shone a spotlight on the working conditions at Amazon. As the company touted its $15 minimum wage, critics pointed out that the company can actually push down wages in the warehousing sector. Reporters have for years investigated claims by employees that the company has higher injury rates than the industry average. (Amazon strongly rebuts these stories.)

As the union vote approached, Jeff Bezos became incensed by negative coverage, according to Recode, and asked for a more aggressive public relations strategy. But what followed seems to have hurt the company’s reputation even more.

On March 24, Amazon executive Dave Clark responded to news of Sanders’ visit to Bessemer by calling his company “the Bernie Sanders of employers.” Rep. Mark Pocan, D-Wis., responded that a progressive workplace doesn’t bust unions or make workers “urinate in bottles,” to which Amazon’s official news account replied, “You don’t really believe the peeing in bottles thing, do you?”

That tweet set off an internet firestorm of memes and critical responses, but more than anything else, it was a lie. The issue of Amazon workers’ peeing in bottles has been well–documented by journalists for years. Within a day of the tweet’s being sent, Vice published photos of the pee bottles provided by workers, and The Intercept published internal documents that showed that the company knew not only that workers pees in bottles, but also that some defecated in bags while on the clock.

Amazon’s aggressive tweets created a news cycle around one of the worst parts of the company’s treatment of workers, but it didn’t stop there. Clark and Amazon’s news account continued responding aggressively to Sanders and Sen. Elizabeth Warren, D-Mass. The corporate Twitter account even responded to Warren’s criticism by saying, “One of the most powerful politicians in the United States just said she’s going to break up an American company so that they can’t criticize her anymore.”

Alabama workers begin vote that could create first Amazon union in U.S.

March 30, 202104:33

It should go without saying that this is an unusual PR strategy for any company, especially one of the largest and most powerful corporations in the world. A worker at Amazon even sent an internal ticket to flag the tweets, fearing that the account had been hacked: “These tweets are unnecessarily antagonistic (risking Amazon’s brand), and may be a result of unauthorized access.” The ticket was closed as “not a technical issue.”

On the same day the union vote ended for workers in Bessemer, Twitter accounts purporting to be those of workers at Amazon fulfillment centers around the U.S. began popping up and tweeting about how great it was to work at the company, how they were able to use the bathroom whenever they wanted and why unions were bad for workers. Yet they also seemed to make mistakes, including one who said she was “barely scraping by” before hastily walking it back in subsequent tweets.

Amazon’s Covid-19 Prime Day offers great deals — but at what price?

It was quickly pointed out that many of the accounts’ display photos were AI-generated or taken from random photos online. Rather than being those of real workers, they were more likely to be parody accounts, which was confirmed when many of them were suspended the next day.

However, the fact that so many people seemed to have been pulled in by the accounts shows that even parody passes for real these days — that’s how ridiculous the company’s denials have been. Amazon has also been running a program since 2018 in which specially chosen “ambassadors” are paid to defend Bezos and the company on Twitter, so it wasn’t a stretch to imagine that these workers were changing their approach like Clark and the corporate account.

The fact that so many people seemed to have been pulled in by the accounts shows that even parody passes for real these days.

As Amazon’s PR disaster plays out, the union votes from the Bessemer facility are being counted by the National Labor Relations Board. If workers vote for a union, it will be despite strong anti-union efforts. Amazon pushed anti-union meetings for workers and hired intimidating off-duty police to watch organizers, and it was even reported to have had local officials change traffic signals, negatively affecting organizing efforts at intersections.

Even if the vote fails, though, the workers’ campaign and the wave of support they’ve received are already inspiring workers at other Amazon fulfillment centers around the country to organize with the hope of unionizing to improve their working conditions.

Amazon has put shareholder profits over worker safety and security for years, but with unions, the workers would have significantly more power to push back. In Europe, for example, where its workforce is unionized, workers still have grievances, but they also have more leverage to force the company to make changes.

Through the pandemic, Bezos’ wealth has soared to around $200 billion. Instead of sharing some of Amazon’s gains with its workers, he has tried to crush nascent worker efforts to band together. No matter what happens in Bessemer, Bezos’ response shows exactly what workers are fighting for.

https://www.theguardian.com/technology/2021/apr/03/amazon-bessemer-union-leaders-labor-movement-us

The fuse has been lit’: union leaders hope Amazon effort will boost support across US

Vote in Bessemer, Alabama, is chance to inform younger generations about the role unions play, labor leaders say

Union organizers outside the Amazon facility in Bessemer. Photograph: Nathan Posner/REX/Shutterstock

Sat 3 Apr 2021 05.00 EDT

Counting is currently under way for the historic union election at Amazon’s warehouse in Bessemer, Alabama, and union organizers and leaders throughout the labor movement are hoping the effort will help galvanize support for workers and unions in the south and across the US.

Tevita Uhatafe, 35, a member of Transport Workers Union of America Local 513 in the Dallas area, was one of several union members and leaders who visited Bessemer to lend their support for the union organizing drive.

“I just wanted to hear workers’ stories, see what was going on there and learn a little bit about what was going on with their lives, as well as what can we do to help these people and support this union effort,” said Uhatafe.

The enthusiasm comes as a pivotal moment for US unions. Joe Biden was elected on a pro-union platform and only this week told a crowd in Pittsburgh: “I’m a union guy. I support unions. Unions built the middle class, and it’s about time they start to get a piece of the action.”

The huge publicity the Amazon vote is attracting is a chance to inform a younger generations that have not received a lot of education on the history of the US labor movement about the role unions have played in Alabama, said Uhatafe.

“I really wanted to show them that there’s a new generation that’s coming up that wants to bring this movement into this generation, and show people that we really do fight for their jobs and for their livelihoods,” he added. “There’s going to be a whole lot of organizing going on if this is successful – even if it isn’t, the fuse has been lit.”

Advertisement

Other labor leaders and workers echoed his sentiments.

“The union drive in Bessemer, Alabama, is going to have a ripple effect,” said Liz Shuler, secretary-treasurer of the AFL-CIO, the largest federation of labor unions in the US. “It’s about so much more than Amazon. It’s about fundamental power and inequality. About a labor movement that’s innovating and organizing on a new frontier to take on issues like data collection, and making progress in the long march for civil rights. And Bessemer is inspiring people all over the country to take collective action with their co-workers. This isn’t the end, it’s a powerful beginning.”

The coronavirus pandemic exposed poor working conditions in industries and jobs where workers are deemed “essential” and praised as “heroes” but often receive wages and benefits that make it difficult for them to make ends meet. The risks posed by Covid-19 often worsened working conditions and heightened concerns about safety protections in places like Amazon warehouses that not only continued operating, but saw surges in demand and profits.

Chris Smalls, who was fired from Amazon’s Staten Island, New York warehouse after organizing a protest at the beginning of the pandemic over Covid-19 safety concerns, has spent the past year participating in actions and speaking out in favor of organizing efforts at Amazon around the US, including in Alabama.

“This is the most important union drive since probably the Great Depression,” said Smalls. “The whole nation is watching this vote. Our hopes no matter which way it goes is that Alabama lights a spark for all of us to start organizing in a city near you. That’s exactly what we intend to do and I support any and all efforts to do so.”

The union drive has drawn support from community leaders, organizers and elected officials around the US, and in the Birmingham, Alabama area. Labor unions, including the Major League Baseball Players Association, NFL Players Association, several members of Congress, celebrities and organizations have publicly endorsed the effort, participated in solidarity rallies in cities around the US, or visited Bessemer. Workers around the world have also posted video messages to publicly announce their support for the unionization effort.

Bernie Sanders speaks at a rally in support of unionization at an Alabama Amazon facility on 26 March. Photograph: Nathan Posner/REX/Shutterstock

“Without unions we would not have the 40-hour work week, vacation days, sick leave, or employee benefits that millions rely on. Unions built the middle class of this country, and have played a historic role in shaping Birmingham and Jefferson county as a whole, granting opportunities to thousands of working families,” said Randall Woodfin, mayor of Birmingham, Alabama, in a statement in support of the union.

“Birmingham has a long history of workers of all races banding together to demand better working conditions, and the unionization effort in Bessemer is a critical chapter in the history of organized labor in our community.”

The Rev Tonny H Algood with the Alabama Poor People’s Campaign explained that history in the south, as industrialization in the southern US grew after the second world war as corporations sought cheap, non-union workforces, and state governments have since characterized themselves as pro-industry.

“The state has sided with corporations every time,” Algood said.

As an example, he cited Jefferson county changing the traffic light patterns outside the Amazon warehouse at the request of the company as union organizers utilized the stop to speak with workers, and the use of local police providing security for the Amazon warehouse.

From Martin Luther King’s launching of the Poor People’s Campaign in 1967, Alabama, especially in the Birmingham area, has a vast history of labor union organizing connected to the civil rights movement. During the 1960s, civil rights activists in Birmingham relied on their labor union relationships to bolster the civil rights movement, such as Col Stone Johnson, who recruited other union members to serve as bodyguards for the homes and churches of local civil rights movement leaders, or Henry Jenkins, a Retail Wholesale Department Store union member and shop steward in Birmingham, Alabama, who faced racist threats and attacks while organizing workers in the area in the 1960s.

An estimated 85% of the workers at the Amazon warehouse in Bessemer are Black, and organizations like Black Lives Matter-Birmingham and union organizers have emphasized these connections through the union effort.

“This type of organizing and collaboration is not new to Alabama. It seems as though Amazon thought that they can come to Alabama and extend this slave labor-like working environment and that would be okay here,” said Celida Soto Garcia, the president of Sweet (Sustainable Water, Energy and Economic Transition) Alabama. “I guess they didn’t read up on history, because that’s never permissible here in our state. Historically it never has been and never will be.”

She expressed disappointment with Amazon’s adversarial response to the union organizing drive, especially given the immense wealth founder Jeff Bezos has accumulated from the company. Throughout the union election process, Amazon has hired expensive anti-union consultants, attempted to delay the election and force an in-person vote, and pushed anti-union messages to workers through texts, posters, ads, emails, a website, captive audience meetings and mailings. Amazon’s union opposition has extended to social media, as executives and its public relations team have repeatedly asserted the company’s union opposition.

“I really expected more from Amazon. We celebrated their arrival here because we expected more from this multibillion-dollar corporation but it seems that they want to move forward with treating our invaluable people here in Alabama like cogs in the machine,” added Soto Garcia. “We’re going to win this for them and we’re not going to stop fighting until we win this for them.”

… we have a small favour to ask. Across the US and around the world, millions rely on the Guardian for independent journalism that stands for truth and integrity. The Guardian has no shareholders or billionaire owner to please, and we invest every penny we earn back into our journalism. Readers chose to support us financially more than 1.5 million times in 2020, joining existing supporters in 180 countries.

With your help, we will continue to provide high-impact reporting that can counter misinformation and offer an authoritative, trustworthy source of news for everyone. With no shareholders or billionaire owner, we set our own agenda and provide truth-seeking journalism that’s free from commercial and political influence. When it’s never mattered more, we can investigate and challenge without fear or favour.

Unlike many others, we have maintained our choice: to keep Guardian journalism open for all readers, regardless of where they live or what they can afford to pay. We do this because we believe in information equality, where everyone deserves to read accurate news and thoughtful analysis. Greater numbers of people are staying well-informed on world events, and being inspired to take meaningful action.

We aim to offer readers a comprehensive, international perspective on critical events shaping our world – from the Black Lives Matter movement, to the new American administration, Brexit, and the world’s slow emergence from a global pandemic. We are committed to upholding our reputation for urgent, powerful reporting on the climate emergency, and made the decision to reject advertising from fossil fuel companies, divest from the oil and gas industries, and set a course to achieve net zero emissions by 2030.

https://www.theguardian.com/technology/2021/mar/30/amazon-twitter-defenders-fake-accounts

‘Fake’ Twitter users rush to Amazon’s defence over unions and working conditions

Similar accounts have been used before during periods when the company was facing increased scrutiny and criticism

‘Many of these are not Amazon FC Ambassadors – it appears they are fake accounts that violate Twitter’s terms. We’ve asked Twitter to investigate and take appropriate action,’ an Amazon spokesperson said.

Wed 31 Mar 2021 02.00 EDT

Last modified on Fri 2 Apr 2021 04.59 EDT

A surge of “fake” Twitter accounts have emerged to defend Amazon and push back against criticism of working conditions at the company amid a fiercely fought union election for the Amazon warehouse in Bessemer, Alabama.

Many of the account handles start with “AmazonFC” followed by a first name and a warehouse designation. The accounts often respond to criticism against Amazon on Twitter, dismissing concerns and reports about robotic working conditions and high injury rates.

One, now suspended, account tweeted: “Unions are good for some companies, but I don’t want to have to shell out hundreds a month just for lawyers!”

Similar accounts have been used before in periods when criticism toward the company went viral in 2018 and 2019. Several of the Amazon Twitter user accounts cited in reports from 2018 and 2019 no longer exist. Others have switched names. Some of the accounts have been exposed as using fake profile pictures from stock photos.

Some Amazon employees act as “ambassadors” – sharing positive experiences of working with the company. The company confirmed that some of the latest tweets allegedly coming from its ambassadors were fake.

“Many of these are not Amazon FC Ambassadors – it appears they are fake accounts that violate Twitter’s terms. We’ve asked Twitter to investigate and take appropriate action,” said an Amazon spokesperson.

The spokesperson did not clarify how many Twitter accounts are run by real Amazon ambassadors, or which accounts still on the platform are actually run by Amazon workers serving as public relations ambassadors. Amazon had declined to provide information on these accounts in previous reports as well, including how these workers are compensated for serving in these roles on social media, though some previous reports have noted these workers work on social media in lieu of warehouse work, and can receive perks such as free gift cards or days off.

The investigative journalism site Bellingcat has compiled a list of at least 56 Amazon FC Ambassador Twitter accounts.

Some of the accounts that became active recently on Twitter, such as @AmazonFCDarla and @AmazonFCLulu were suspended by Twitter. In response to the accounts, some Twitter users created obvious parody accounts mocking the robotic defenses of Amazon and uniform design of the accounts.

Amazon’s public relations tactics have received scrutiny over the years, and more so recently after the Amazon CEO Dave Clark and the Amazon News Twitter account criticized senators Bernie Sanders and Elizabeth Warren and Congressman Mark Pocan on Twitter. These attacks backfired after leaked memos to The Intercept revealed Amazon engineers flagged the tweets over concerns the account may be compromised and characterized the tweets as “unnecessarily antagonistic (risking Amazon’s brand).”

Other leaked memos also revealed Amazon managers had complained about Amazon delivery drivers leaving bottles of urine and bags of feces in trucks, after Amazon’s PR account claimed reports of workers urinating in bottles were false. NBC News also reported the National Labor Relations Board is currently determining whether to consolidate multiple complaints from workers over the past year alleging interference from Amazon against workers’ attempts to organize or form a union.

On 30 March, Amazon’s senior vice-president for policy and communications, Jay Carney, a former Obama Administration staffer, joined in on the pushback against high profile critics like Sanders. The recent uptick in Amazon’s public relations team and executives antagonizing critics reportedly stems from complaints from Amazon founder Jeff Bezos himself, who recently complained to other Amazon executives they weren’t pushing back on their critics enough.

https://www.vox.com/recode/2019/12/11/20982652/robots-amazon-warehouse-jobs-automation

How robots are transforming Amazon warehouse jobs — for better and worse

Amazon is leading a robotics race that will have a seismic impact on the warehouse industry, which employs more than 1.1 million Americans today.

By Jason Del Rey@DelRey Dec 11, 2019, 8:00am EST

When the tech industry has come up in the 2020 Democratic presidential debates, the most important discussion topic hasn’t been about breaking up the tech giants; it’s been about the automation of jobs and the massive impact this is expected to have on the US labor force.

A woman uses a computer to control robots at the 855,000-square-foot Amazon fulfillment center in Staten Island, New York on February 5, 2019. Johannes Eisele/AFP/Getty Images

At the center of this debate is Amazon, a company that employees hundreds of thousands of employees in its massive warehouse network, which is also a company whose investment in robots and other automation technologies means it could one day be a huge job eliminator, too.

In 2012, Amazon spent $775 million to purchase a young robotics company called Kiva Systems that gave it ownership over a new breed of mobile robots that could carry shelves of products from worker to worker, reading barcodes on the ground for directions along the way.

Open Sourced is Recode by Vox’s year-long reporting project to demystify the world of data, personal privacy, algorithms, and artificial intelligence. And we need your help. Fill out this form to contribute to our reporting.

Today, Amazon has more than 200,000 mobile robots working inside its warehouse network, alongside hundreds of thousands of human workers. This robot army has helped the company fulfill its ever-increasing promises of speedy deliveries to Amazon Prime customers.

“They defined the expectations for the modern consumer,” said Scott Gravelle, the founder and CEO of Attabotics, a warehouse automation startup.

And those expectations of fast, free delivery driven by Amazon have led to a boom in the retail warehouse industry, with entrepreneurs like Gravelle and startups like Attabotics attempting to build smarter and cheaper robotic solutions to help both traditional retailers and younger e-commerce operations keep up with a behemoth like Amazon.

This robotics race — led by Amazon — will have a seismic impact on the warehouse industry, which employs more than 1.1 million Americans today. And the rise of these artificially intelligent robots means there’s likely a day coming when these warehouse robots will be capable of replacing just about every human task, and human worker.

“The thing that really makes us unique as human beings is our ability to solve problems,” Martin Ford, author of The Rise of Robots, told me this summer for an episode of the Land of the Giants: The Rise of Amazon podcast. “Machine learning and related technologies are for the first time allowing machines to do that and to compete with that capability. That’s really kind of a game-changer.”

In the meantime, robots have the potential to eliminate some of the most menial warehouse labor, as evidenced by the Amazon robots that now transport products across massive warehouses in place of workers who used to be forced to walk the equivalent of 10 or more miles a day.

That sounds like a good thing, but new research indicates these robots may be increasing worker injury rates, even though they’re taking on some of the hard labor.

Here’s a look at the good and the bad of the rise of robots inside of Amazon, and a peek ahead at where this is all headed.

The good

If you’ve heard stories of Amazon warehouse workers walking 10 to 20 miles a day on hard concrete floors, well, they’re true. But in newer warehouses outfitted with robots, much of that walking has been eliminated.

“Walking 12 miles a day on a concrete floor to pick these orders. … If you’re not 20 years old, you’re a broken person at the end of the week,” said Marc Wulfraat, founder and president of the supply chain consultancy MWPVL International.

The type of employees that used to do the walking — some called “stowers,” others called “pickers” — now remain stationary, standing at their own work stations, with cushion pads beneath their feet, if they are working in one of the robotic warehouses.

Stowers in older Amazon facilities used to walk up and down long aisles pushing a cart full of products, placing them randomly on shelves where they found space, and scanning them with a handheld device to mark their location in a system.

Now Amazon robots carry empty shelving units — known as pods — to the workstations of stowers, who take products placed in front of them and fit them into open shelf space inside the shelving pods.

When the pod is full, the stower presses a button that sends the robot and attached shelving unit rolling across a caged-in area of the warehouse, and eventually to the workstation of a “picker.”

Like stowers, pickers in older facilities walked miles on end each day, plucking a product off a shelf, scanning it, and placing it into a cart they pushed the whole way. But, they, too, now remain standing at their own workstation in Amazon’s robotic warehouses, plucking items off of shelving units that robots carry right to them.

“Having a rubber mat, where goods come to you, is three times more productive than the traditional approach and it is more humane on the people who work in these fulfillment centers,” Wulfraat said.

An Amazon spokesperson said these new technologies help the company store up to 40 percent more inventory in their warehouses, and that they make employees’ jobs easier.

The bad

“But picking three times faster also implies more wear and tear due to repetitive motion and working faster at lifting and handling products,” Wulfraat added.

So along with the drive to automate more warehouse tasks, comes much higher expectations for workers.

“The robots have raised the average picker’s productivity from around 100 items per hour to what Mr. Long and others have said is a target of around 300 or 400, though the numbers vary across teams and facilities,” the New York Times reported in July.

An Amazon spokesperson did not comment on the specific goals, but said the company provides coaching to those struggling to meet goals.

The new targets, though, mean that workers are allowed just a handful of seconds between each product task, which can be complicated by the 8-foot-tall shelving units that the robots carry to the stations of pickers and stowers, Wulfraat said. Because of that height, each worker has a stepladder that they occasionally need to ascend to place or retrieve products from the top row of the shelving units.

“Workers who stow items are supposed to keep lightweight products at the top or bottom of the pod and heavy products between the chest and the knees,” Wulfraat said. “But it’s not possible to adhere to this when the work is happening so fast and people are under the gun, so people take safety and ergonomic shortcuts out of necessity.”

Men work at a distribution station in the 855,000-square-foot Amazon fulfillment center in Staten Island, on February 5, 2019. Johannes EiseleI/AFP/Getty Images

Such shortcuts mean that the pickers on the receiving end have to sometimes carry heavier-than-designed items down the steps of their stepladder, resulting in a “higher probability” of injury, according to Wulfraat.

A recent investigation by the Center for Investigative Reporting’s Reveal group, and published in the Atlantic, appeared to show that the rate of worker injuries at Amazon’s robotic warehouses is in fact higher than those facilities in which robots are not in use.

“Of the records Reveal obtained, most of the warehouses with the highest rates of injury deployed robots,” the piece read.

“After Amazon debuted the robots in Tracy, California, five years ago, the serious-injury rate there nearly quadrupled, going from 2.9 per 100 workers in 2015 to 11.3 in 2018, records show,” the piece added.

The Amazon spokesperson said in an email that the health and safety of Amazon employees is a top priority, and listed several initiatives to try to back that up. She also said Amazon is more aggressive than others in the industry when it comes to documenting injuries, insinuating that’s why Amazon injury rates may be higher than industry norms.

Still, experts who study the robotics industry and its impact on workers fear that the squeezing of human workers is a feature — not a bug — of this period bridging workplaces to a fully-automated future.

“The kind of efficiency that Amazon has to have in order to operate the way it operates now and also to do what it wants to do in the future. … They’ve got to get more and more efficient,” Ford, the author, said. “Now as long as people are still part of the loop, what that means is that the whole system has to effectively come under more and more algorithmic control.”

He continued: “So in a sense, if you’re one of these workers in that environment, you’re truly just going to be kind of a cog in the machine. You’re gonna be sort of a plug-in neural network as a human being that is performing some tasks that right now the robots can’t.”

What’s next

Amazon continues to add versions of the original Kiva robots to more and more fulfillment centers. At the same time, the company works on new robotic inventions to handle new tasks inside its facilities.

Reuters reported in May that Amazon was rolling out automated packing machines in some of its warehouses.

The company has also started introducing new mobile robots — similar in appearance to the original Kiva ones — to shuttle packages around inside sortation centers, which are mini-warehouses where packaged customer orders are sorted by geographic destination.

In these same facilities, Amazon is also experimenting with giant robotic arms that would place the ready packages onto the mobile robots.

All the while, Amazon continues to chase the Holy Grail of warehouse robotics: a robot that can grasp a wide range of merchandise types — with different shapes, sizes, and form factors — with a level of dexterity that’s similar to what the human hand can do.

A company spokesperson confirmed that it’s an area that Amazon is interested in and continues to research.

Such an invention, though, could mean Amazon would need fewer workers working as pickers and stowers, too.

In past years, Amazon has sponsored a contest where robotics teams from around the world have competed to create the best robot picker. More recently, Amazon has decided to fund research from external teams instead of hosting the event.

CEO Jeff Bezos said earlier this year that the robotic grasping problem will be solved in the next decade. But some logistics and robotics experts think that certain types of Amazon merchandise could be picked by robots years sooner than that.

And Amazon has indirectly hinted at this, too. This year, the company announced plans to “upskill” 100,000 of its US employees, including warehouse workers. A spokesperson said that as a top US employer, the company feels a responsibility to help employees develop new technical skills to move into better-paying jobs.

In a press release, Amazon cited a “changing jobs landscape” as the impetus for the job-training push.

It could have easily used the word “automation” instead.

Open Sourced is made possible by the Omidyar Network. All Open Sourced content is editorially independent and produced by our journalists.

https://www.wired.com/story/amazon-warehouse-robots/

Inside the Amazon Warehouse Where Humans and Machines Become One

In an Amazon sorting center, a swarm of robots works alongside humans. Here’s what that says about Amazon—and the future of work.

AMAZON

THEY CALL ME the Master of Robots—or at least they should. I grab a flat package, hold its barcode under a red laser dot, and place it on a small orange robot. I hit a button to my left and off zips the robot to do my bidding, bound for one of more than 300 rectangular holes in the floor corresponding to zip codes. When it gets there, the bot engages its own little conveyor belt, sliding the package off its back and down a chute to the floor below, where it can be loaded onto a truck for delivery.

This is not an experimental system in a robotics lab. These are real packages going to real people with the help of real robots in Amazon’s sorting facility of tomorrow, not far from the Denver airport. With any luck, my robot friend and I just successfully shipped a parcel to someone in Colorado. If not—well, blame the technology, not the user.

Seen from above, the scale of the system is dizzying. My robot, a stubby mobile slab known as a drive (or more formally and mythically, Pegasus), is just one of hundreds of its kind swarming a 125,000-square-foot “field” pockmarked with chutes. It’s a symphony of electric whirring, with robots pausing for one another at intersections and delivering their packages to the slides. After each “mission,” they form a neat queue at stations along the periphery, waiting for humans to scan a new package, load the robots once again, and dispatch them on another mission.

You don’t have to look far to see what a massive shake-up this is for the unseen logistics behind your Amazon deliveries. On the other side of the building are four humans doing things the old way, standing at the base of a slide flowing with packages. Frenetically they pick up the parcels, eyeball the label on each, and walk them over to the appropriate chutes. At the bottom of the chutes, yet more humans grab the packages and stack them on pallets for delivery. It’s all extremely labor-intensive and, in a word, chaotic.

Amazon needs this robotic system to supercharge its order fulfillment process and make same-day delivery a widespread reality. But the implications strike at the very nature of modern labor: Humans and robots are fusing into a cohesive workforce, one that promises to harness the unique skills of both parties. With that comes a familiar anxiety—an existential conundrum, even—that as robots grow ever more advanced, they’re bound to push more and more people out of work. But in reality, it’s not nearly as simple as all that.

If only the Luddites could see us fulfilling online orders now.

THIS COLORADO WAREHOUSE is, in a way, a monument to robots. It’s not one of the Amazon fulfillment centers you’ve probably heard of by now, in which humans grab all the items in your order and pack them into a box. This is a sorting facility, which receives all those boxes and puts them on trucks to your neighborhood. The distinction is important: These squat, wheeled drives aren’t tasked with finely manipulating your shampoos and books and T-shirts. They’re mules.

Very, very finely tuned mules. A system in the cloud, sort of like air traffic control, coordinates the route of every robot across the floor, with an eye to potential interference from other drives on other routes. That coordination system also decides when a robot should peel off to the side and dock in a charger, and when it should return to work. Sometimes the route selection can get even more complicated, because particularly populous zip codes have more than one chute, so the system needs to factor in traffic patterns in deciding which portal a robot should visit.

It’s basically a very large sudoku puzzle,” says Ryan Clarke, senior manager of Special Amazon Robotics Technology Applications. “You want every column and every row to have an equal amount of drops. How do we make sure that every row and every column looks exactly equal to each other?” The end goal is to minimize congestion through an even distribution of traffic across the field. So on top of tweaking the robots’ routes, the system can actually switch the chute assignments around to match demand, so that neither the robots nor the human sorters they work with hit any bottlenecks.

To map out all this madness, Amazon runs simulations. Those in turn inform how the drives themselves should be performing. What’s the optimal speed? What’s the optimal acceleration and deceleration, given you want the deliveries to be as efficient as possible while keeping the robots from smashing into one another? After all, a bump might toss a package to the ground, which other robots would spot with their vision sensors and route around, adding yet another layer of complexity to the field. (The robots have sensors on either end of their conveyor belt, by the way, so if a package starts to slip off the side, the belt automatically engages to pull the package back on.)

Amazon runs complex simulations to coordinate the robots on the field.

AMAZON

The temptation might be to get these machines moving as quick as possible. “But it would be like having a Ferrari in downtown San Francisco—all you’re doing is stop and go,” says Clarke. “We looked at tuning it to many different parameters and found that more speed and more acceleration actually had a reverse effect. They were just bumping into each other and causing more pileups.”

Ready for more complexity? Amazon had to tweak the built space itself to keep the machines happy. Humans doing things the old way on the other side of the building, for instance, enjoy basking in the photons that pour through skylights. Above the robots’ field, though, the skylights are covered, because the glare might throw off the machines’ sensors. To navigate, they’re using a camera on their bellies that reads QR codes on the ground. Even the air-conditioning units hanging from the roof are modified. On the human side, they blow air straight downward, but above the robots they blow out to the side, because gusts of air could blow light packages off the machines’ conveyor belts.

The WIRED Guide to Robots

Worse yet, precarious packages like liquids could send the system into chaos. So although the system is automated, humans still monitor the robots on flatscreens below the field, where the packages come down the chutes, and respond to crises. “Think about if I had a package and it had a gallon of paint in it, and that gallon of paint was damaged and it leaked down one of these chutes,” says Steve McDonnell, general manager of the sorting center. “Within minutes I’m able to shut that chute off, redirect drives to another chute, and I’m done.”

Most Popular

The key here is flexibility—not a word that first comes to mind when you think of robots. Flexibility in the robots’ pathways, in their destinations, in the number of robots on the field at once. You might, for example, think the more machines out there, the better. Amazon could deploy up to 800 drives simultaneously, but that could jam up the floor like traffic in a city. Instead, they’re typically operating 400 or 500, with others parked off to the side and waiting to be circulated in.

Beyond coordinating the robots themselves, there’s the question of how to make them good coworkers for the human employees. The humans’ job is to place packages in 6-foot-tall boxes below the field, taking care not to toss in heavy packages first. To make that work manageable, the robots have to distribute packages between the multiple chutes for a particular zip code, so a given chute doesn’t overflow. At the same time, the system considers how to best group packages downstairs by their departure time, so workers don’t have to run around hunting for them.

“The interaction between the associate and the drives is almost like a 3D chess set,” says McDonnell, “because you can optimize the drive field, but then you can make the associate’s job harder below the field.”

ACROSS THE FIELD from the human workers distributing packages to the drives, a prototype robotic arm, named Robin, sits at the end of a conveyor belt. Its “hand” is a vacuum manipulator, designed to snag boxes and flat packages.

This robotic arm is a test of what it might look like to further automate the work of shuffling packages around. The idea is that the conveyor will deliver packages to the arm, which would then load the drives. “We’re going to feed it a little bit differently than we do with humans,” says Rob Whitten, senior technical program manager. “We’re not going to just give it a pile coming down a chute—we’re going to kind of toss it softballs. We’re going to give it a little more structure so it can handle it.” For parcels it can’t manipulate, like if they’re too heavy or weirdly shaped, humans would step in to help.

As I walk down the line of human robot-loaders, I come across a worker who has set aside a broken box, which has spilled out bottles and other entrails. That uniquely capable human could do two things here: use his problem-solving skills to say, “Something is wrong, I need to set these aside,” and then manipulate those objects with exceedingly fine motor skills.

This robot arm has neither problem-solving prowess nor fine motor skills. Imagine if clear laundry liquid had broken inside a package and soaked the bottom of the box. A human might smell the detergent or feel its stickiness before they see it. A robot arm relying on sight alone would miss the problem, loading the package on a drive robot that then snail-slimes the floor of the field.

Even if they had some semblance of judgment, robots are still awful at manipulating complex objects like bottles. That’s why Amazon is keeping it simple here, with a suction arm meant to stick to flat surfaces, as opposed to an analog of the human hand. For quite some time, humans will need to (nearly) literally hold these robots’ hands.

THE BOTTOM LINE is this: We humans have to adapt to the machines as much as the machines have to adapt to us. Our careers depend on it.

Amazon runs simulations to figure out how to keep their human workers comfortable when loading robots with packages. This includes their range of movement from an ergonomics standpoint and their safety. Or such questions as how best for a human to grab a parcel, scan it, place it, and reach over to hit the button that sends the robot on its way. “There’s an art to making it feel seamless between what the robot is doing and what the humans are doing,” says Brad Porter, VP of robotics at Amazon.

It’s the kind of dynamic environment that’s perfect for the development of Amazon’s next iteration of its system. The company is working on a new modular robot called Xanthus with different attachments, say to hold containers instead of using a conveyor belt. This machine will in a sense bridge the divide between fulfillment centers, where humans are loading products into boxes by hand, and sorting centers, where they’re mostly working with those assembled boxes.

Amazon’s new modular Xanthus robot can be outfitted with attachments that allow it to carry different kinds of cargo.

AMAZON

“You can see how combined with maybe the addition of a sensor platform, you could have an autonomous drive that’s driving totes around,” says Porter. But you can also take that same thin sled and replace the tote-carrying unit with a conveyor top and deploy it in the sorting center.

Herein lies Amazon’s huge advantage: It’s got the funds and the talent to develop robots in-house, tailoring each to solve problems specific to Amazon. Other warehouses are starting to go robotic, but they’re working with other companies’ machines. For instance, Boston Dynamics—maker of the hypnotically impressive SpotMini and Atlas—will soon offer a box-lifting robot called Handle. But it’s a generalist machine, not developed exclusively for one client.

Amazon, on the other hand, can iterate on a robot until it’s perfectly adapted for a specific task. “They’re building it for themselves, and they’re building it for their environment and circumstances,” says John Santagate, research director of service robotics at IDC, which does market research. “It’s hard to build any one product that suits all of it.”

And every worker they hire into a machine-facing role is doing something no other human has ever done before—lower-level workers in this facility have been promoted to help oversee the massive system whirring around them, as well as the humans intimately integrated with it. “The fully automated or highly automated fulfillment center isn’t a North Star we’re trying to hit,” says Porter. “Do we see additional levels of automation, at higher and higher levels? Yeah, I think that will increase as the capabilities of our systems increase.”

Here’s the big question, though. Is this kind of automation bound to replace human jobs entirely, or replace parts of those jobs? “Most of the research seems to suggest that the direction that automation is moving in is the displacement of skills, not jobs,” says R. David Edelman, formerly President Obama’s special assistant on the digital economy, and now the director of MIT’s Project on Technology, Economy, and National Security. “That suggests those individuals can, by Amazon, be reskilled or leverage other skills they already have in the same job.”

These days, industries that are short human labor need automation to survive. Consumers still want fresh produce, but California’s farms are facing a labor shortage of 20 percent and are increasingly turning to agricultural robotics. Amazon’s business is booming, yet America is enjoying historically low unemployment, so laborers have lots of options for work. “The demand on that company is increasing, but the availability of resources to fill that demand isn’t necessarily increasing,” says Santagate. “In fact it’s probably contracting.” Robots are filling the void.

Here in this sorting center of tomorrow, I walk along the edge of the field and hear the morning break for humans, called out on loudspeakers. The drive robots continue to shuffle around for a few minutes, with their incessant electric white noise, until suddenly the place falls almost silent. Having delivered their packages to chutes, the robots have run out of work. They park off to the side of the field, some of them in charging stations. Only when the loudspeakers call the end of break do the machines start up again, ready for their humans to feed them more packages.

If only the Luddites could see our codependency now.

Amazon Has Turned a Middle-Class Warehouse Career Into a McJob

Despite a starting wage well above the federal minimum, the company is dragging down pay in the logistics industry and bracing for a fight with unions.

Many Amazon warehouse employees struggle to pay the bills.

Photographer: Victor J. Blue/Bloomberg

By Matt Day and Spencer Soper

December 17, 2020, 5:00 AM EST

Amazon.com Inc. job ads are everywhere. Plastered on city buses, displayed on career web sites, slotted between songs on classic rock stations. They promise a quick start, $15 an hour and health insurance. In recent weeks, America’s second-largest employer has rolled out videos featuring happy package handlers wearing masks, a pandemic-era twist on its annual holiday season hiring spree.

Amazon’s object is to persuade potential recruits that there’s no better place to work.

The reality is less rosy. Many Amazon warehouse employees struggle to pay the bills, and more than 4,000 employees are on food stamps in nine states studied by the U.S. Government Accountability Office. Only Walmart, McDonald’s and two dollar-store chains have more workers requiring such assistance, according to the report, which said 70% of recipients work full-time. As Amazon opens U.S. warehouses at the rate of about one a day, it’s transforming the logistics industry from a career destination with the promise of middle-class wages into entry-level work that’s just a notch above being a burger flipper or convenience store cashier.

Union workers who make comfortable livelihoods driving delivery trucks and packing boxes consider Amazon an existential threat. While labor tensions have simmered for years, the stakes have risen sharply amid the pandemic, which prompted Amazon to hire more than 250,000 people to keep up with surging demand from home-bound shoppers. Risking infection while toiling in a crowded warehouse for $15 an hour has many Amazon workers asking if they’re getting shortchanged.

A Bloomberg analysis of government labor statistics reveals that in community after community where Amazon sets up shop, warehouse wages tend to fall. In 68 counties where Amazon has opened one of its largest facilities, average industry compensation slips by more than 6% during the facility’s first two years, according to data from the Bureau of Labor Statistics. In many cases, Amazon quickly becomes the largest logistics player in these counties, so its size and lower pay likely pull down the average. Among economists, there’s a debate about whether the company is creating a kind of monopsony, where there’s only one buyer—or in this case one employer.

While Amazon’s arrival coincides with rising pay in some southern and low-wage precincts, the opposite is true in wealthier parts of the country, including the northeast and Midwest. Six years ago, before the company opened a giant fulfillment center in Robbinsville, New Jersey, warehouse workers made $24 an hour on average, according to BLS data. Last year the average hourly wage slipped to $17.50.

Wages often tick higher in subsequent years, but don’t reach their pre-Amazon level till five years after a new facility opens—meaning that industry workers, on average, find themselves no better off half a decade after Amazon’s arrival.

“Bloomberg’s conclusion is false—it violates over 50 years of economic thought, and suspends the law of supply and demand,” a company spokesperson said in an emailed statement. “Hiring more, by paying less, simply does not work. Many of our employees join Amazon from other jobs in retail which tend to be predominantly part-time, reduced benefit jobs with substantially less than our $15 minimum wage. These employees see a big increase in pay per hour, total take-home pay, and overall benefits versus their previous jobs. What surprises us is that we are the focus of a story like this when some of the country’s largest employers, including the largest retailer, have yet to join us in raising the minimum wage to $15.”

Amazon Workers Need Help Buying Food

Companies with the most employees receiving government food vouchers through the Supplemental Nutrition Assistance Program (SNAP).

Source: Government Accountability Office

Employees receiving support from the Supplemental Nutrition Assistance Program in Arkansas, Georgia, Indiana, Maine, Massachusetts, Nebraska, North Carolina, Tennessee and Washington.

Chief Executive Officer Jeff Bezos, whose wealth grew about 65% this year as his company posted record sales and profits, has so far managed to keep unions out of his U.S. operations. Now that’s being challenged. In November, representatives of the Retail, Wholesale and Department Store Union quietly filed paperwork with the National Labor Relations Board, proposing to form a union on behalf of 1,500 workers at Amazon’s Bessemer, Alabama, fulfillment center. On Wednesday, the NLRB gave workers the greenlight to put the proposal to a vote, which promises to be the biggest referendum to date on the retail giant’s fraught relationship with its frontline workers.

“The concern isn’t so much ‘the robots are coming, and they’re going to put everybody out of work,’” says Ben Zipperer, an economist with the Economic Policy Institute. “It’s more that the jobs being created by extremely profitable companies have either poor pay or poor working conditions, or are not the kind of jobs that you would expect an extremely rich country, and rich company, to be able to provide.”

Breaking down pallets or hauling cartons of lettuce is hardly the stuff of American business mythology. Warehouses, featureless rectangles located in exurbs and commercial districts, are far from the plant-filled orbs and office perks of Amazon’s Seattle headquarters. But for many Americans, the logistics industry has long provided a path into the middle class, particularly for those who didn’t attend college.

Warehouses have typically paid less than factories but more than retailers. These haven’t been highly skilled jobs, but do require a certain level of ability—whether managing inventory or driving a forklift without damaging goods and hurting anyone. As recently as the early aughts, municipal officials in southern California looking to replace vanishing aerospace manufacturing jobs settled on the logistics industry, believing it would give lower-skilled workers the opportunity to move up.

Since then, industry wages have come under pressure amid a push to carry less inventory and to subcontract work to lower-cost middlemen. But logistics really started to change with the rapid acceleration of e-commerce. And no company has done more to reshape how products are warehoused, packed and shipped than Amazon, with its strong focus on customer service.

Shipping orders directly to consumers from an inventory of millions of products required redesigning not just the physical buildings but the jobs of the people working inside. After 20 years of trial and error, Amazon has turned its fulfillment centers into finely tuned assembly lines, often grueling workplaces that have been the subject of frequent media reports over the years, including investigations probing injury rates and pay practices.

Courtenay Brown at her home in Newark, on Wednesday, Dec. 16, 2020. Brown says she was homeless for a while during her time working for Amazon.

Photographer: Gabriela Bhaskar/Bloomberg

Most of the labor in Amazon’s largest fulfillment centers is divided into simple, repetitive tasks: receiving goods arriving in trucks, placing items into mesh shelving, or retrieving and speeding them along a conveyor belt in yellow plastic bins to be boxed and shipped. Most jobs are marketed to high-school graduates—no resume required, start as soon as next week—who spend 10-hour shifts standing at a single station, cogs in a giant machine built for speed and efficiency. Workers receive about one day of training and are put on the line to see if they have what it takes.

Matt Giannini, who spent five years at a warehouse in New Jersey, says Amazon’s genius lies in simplifying most tasks to the point but where anybody can do it. “They’ve gotten it to such a science,” he says. “Every single process is very simple.”

But job satisfaction can be elusive when most workers are interchangeable cogs. Quality of life in the warehouse, Giannini says, often breaks along a very simple divide: people who spend their days standing by a computer terminal that tracks their every move, and those with less scrutiny and more freedom.

Amazon’s Arrival Means More Jobs, Lower Pay

Average warehouse industry wages fall at first in counties where Amazon opens new facilities, and only reach their pre-Amazon level five years later.

Bureau of Labor Statistics QCEW (wages), MWPVL International (warehouse locations)

Bloomberg interviewed 42 employees in 20 states. Some enjoy the work and say news reports of workplace travails can be overblown. Many joined to get health insurance, a rare perk for entry-level jobs, and came to Amazon from lower-wage employment in retail or logistics.

But most say there’s little opportunity to move up in a highly automated environment where a handful of people per shift oversee an entire facility. One worker in the Midwest was hoping to rise quickly because he had previous management experience. “It’s the greatest company in the world right now,” he recalls thinking. “I’m going to be able to get in there and move up.” Three years later he’s still at the entry level, picking items.

Amazon touts a training program for promising workers and says it issued more than 35,000 promotions in its logistics operation this year. Ron Delosreyes, who joined Amazon in 2018, says the first step up added responsibility and no raise. But today he’s a salaried supervisor at a Staten Island, New York, warehouse. “I’d like to stay and keep advancing my career,” he says. “Up and up.”

“The last thing we want to do is lose our job because we’ll go back to being homeless and have nothing.”

While 35,000 promotions sounds like a lot, it represents 3.5% of the more than 1 million people who worked in Amazon’s logistics group this year. That’s well below the 9% promotion rate for the industry, as calculated by the payroll processing firm ADP.

Many Amazon workers quit or are fired for safety and productivity infractions within a year or two of starting—a high rate of turnover even in an industry where people change jobs frequently. Studies have shown worker churn rises when Amazon moves to town. And workers say the company does little to encourage long tenure.

The relative few who do last more than a year or two often struggle economically.

Courtenay Brown was hired at an Amazon grocery distribution hub in Avenel, New Jersey, three years ago. For several months after joining Amazon, she and her sister, who also works there, were homeless, bouncing from one motel to another while trying to save a deposit for an apartment. They found places they could afford, but landlords denied their applications because they didn’t make enough, she says. With motel rooms eating up about $600 a week, the sisters missed meals and slurped down free coffee and cocoa at work. Eventually, a charity paid their first month’s rent and security to get them established in their current apartment. Brown, 30, was excited to have a washing machine to rid her clothes of the cigarette smell that often permeated the motels.

About half of her take-home pay covers her share of the rent. The balance mostly covers food, utilities and the cost of commuting, which includes frequent $50 Uber rides when she has to work late and misses the final van shuttle home. Brown pays about $200 a month for the van shuttle. She usually arrives at work at 5:30 am and works until close to 6 pm. She spends her vacation time doing errands or resting at home in her pajamas because she can’t afford to go anywhere.

Brown finally got the promotion she’d been hoping for in the fall and a $2 hourly raise, but it will last only through the holiday season while she helps train new workers and open facilities. She’ll find out in January if she goes back to her old job and previous pay rate of about $17 per hour or if Amazon has a permanent promotion for her.

“Me and my sister, the last thing we want to do is lose our job because we’ll go back to being homeless and having nothing,” says Brown, who joined community groups advocating for Amazon workers despite colleagues’ warnings she could be fired for speaking out. “We’re in a tough situation, and this is all we can find that’s stable. Amazon comes to places when people are desperate.”

Similar jobs at unionized logistics companies typically pay twice as much—enough for workers to pay the bills and save.

Joey Alvarado at his home in Moreno Valley, California.

Photographer: Elisa Ferrari/Bloomberg

Joey Alvarado, 42, makes almost $30 an hour moving boxes filled with pet food, shampoo, canned goods and other items sold by Stater Bros. Markets, a southern California supermarket chain. His wife stays home with their three children, and the family eats out twice a week, has a boat called Penny Lane and a travel trailer. They vacation on Lake Havasu and the Colorado River. They’re buying a 2,000-square-foot home on half an acre about 30 minutes from the San Bernardino warehouse where he works. Down the street is an Amazon warehouse where people earn far less. “I don’t see how a big company like Amazon can be so greedy,” he says. “The CEO is already a billionaire. What does he want to be a trillionaire? It’s just greed.”

Alvarado belongs to the Teamsters Local 63, which he sees as the difference between what he is paid and what Amazon workers are paid. He has been on the job 19 years and plans to remain. He doesn’t pay any premiums for medical benefits for himself and his family members and has a pension. “This job, you bust your butt, but you get paid,” he says. “No one leaves. You’d be stupid to leave.”

Jeff Fretz, 49, was working part time for United Parcel Service Inc. and attending community college to pursue a career in law enforcement. A full-time UPS truck driving job opened up, and he picked that over becoming a cop. Now he spends his days maneuvering trailers around a UPS warehouse in Bethlehem Township, Pennsylvania, and looks forward to retiring and moving south in seven or eight years with a Teamster’s pension. The job gave him a stable income and good life. He owns a home in Easton and took vacations with his wife and son in Cape May.

Fretz gets disgusted hearing about working conditions at Amazon because UPS pays its workers so much more and is still a profitable company. “A human body is not a machine,” he says. “I can’t do now what I did when I was 25. Working in a union shop protects you for a career.”

“I thought Amazon was more like a Google. But nah, it didn’t go like that.”

Now the unions fear that Amazon will do to the delivery business what it did with warehousing. The number of Americans employed as delivery drivers and couriers, outside of U.S. Postal Service work, has surged by 22% in the last two years, driven partly by the expansion of Amazon’s nationwide network of contract delivery firms and partly by the advent of new grocery delivery services. Wages in the industry fell last year by half a percentage point, the biggest decline in more than 20 years, according to BLS data.

Amazon, which has long sought to reduce its dependence on UPS, Federal Express and the U.S. Postal Service, now ships most of its own customer orders. Many of those deliveries are handled by Amazon’s network of delivery service partners, contract firms that work exclusively for Amazon and lease the trademark blue delivery vans. Driver salaries average $16 an hour, according to recruiting sites, a couple bucks an hour less than the national average for frontline delivery service workers, and roughly half the pay package of an experienced UPS driver.

Amazon also borrowed the gig-economy tactics pioneered by Uber with Flex, a service that relies on people making deliveries in their own vehicles. The idea was to boost delivery capacity without having to buy thousands of vehicles and hire people. Drivers download the Amazon Flex app and can accept assignments that typically pay about $50 for three hours. Once they factor in the cost of a vehicle and fuel, drivers say, the pay is closer to minimum wage.

UPS started a similar service for seasonal work a year after Amazon. But the drivers are employees, get 57 cents per mile, a $5 daily smartphone stipend and belong to the Teamsters union. One driver says he can easily earn $1,800 a month working part time, about 80% more than he ever made doing Flex routes. He can also count on regular work rather than competing against other Flex drivers, who spend hours watching their phones in the hopes of getting work that sometimes never materializes. The seasonal UPS job is a step up for Amazon Flex drivers. UPS’s full-time drivers see it as a step down, depriving them of overtime and potentially undermining their wages.

They have reason to be worried. Amazon’s growth in the logistics industry is undermining union clout. Union membership in transportation and warehousing dropped to 16.1% in 2019 from 21.3% a decade earlier, by far the biggest decline of any industry, according to BLS data. The slide was driven by the rapid growth of non-union jobs at places like Amazon, not a loss of union work.

Now, the RWDSU, an activist unit of the United Food and Commercial Workers union, is campaigning to organize the Alabama facility, which opened in March. A website for the union drive says employees are seeking safer working conditions and protections from arbitrary dismissal, among other things. “I thought Amazon was more like a Google,” one employee says in a video posted to the site. “The bigger the company, the more benefits, the more loyalty to the worker. But nah, it didn’t go like that.”

Now that the federal labor regulator has approved the union’s proposal, a vote is likely some time next year.

Unfulfilled promises Amazon fulfillment centers do not generate broad-based employment growth

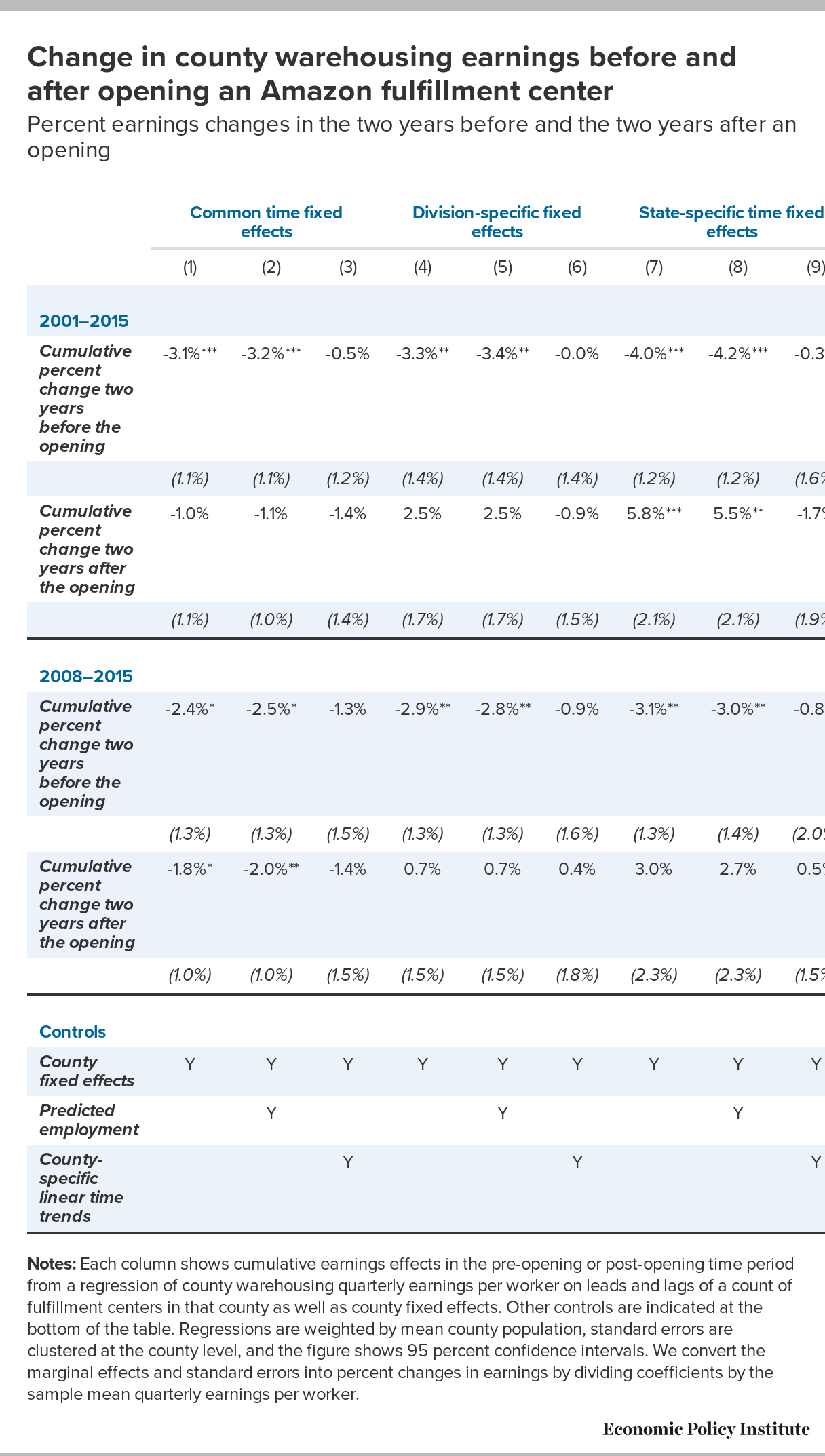

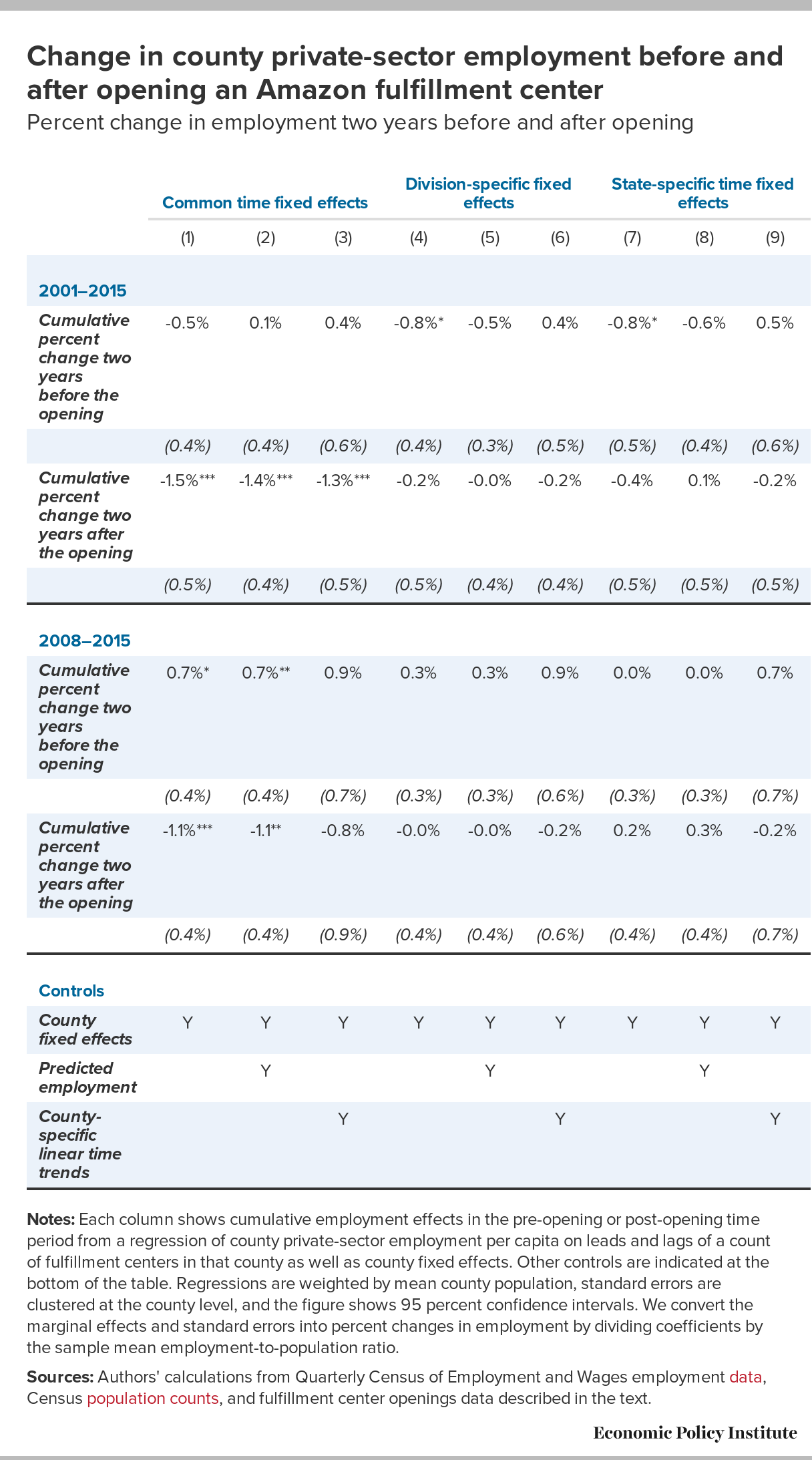

Report • By Janelle Jones and Ben Zipperer • February 1, 2018

What this report finds: When Amazon opens a new fulfillment center, the host county gains roughly 30 percent more warehousing and storage jobs but no new net jobs overall, as the jobs created in warehousing and storage are likely offset by job losses in other industries.

Why it matters: State and local governments give away millions in tax abatements, credits, exemptions, and infrastructure assistance to lure Amazon warehouses but don’t get a commensurate “return” on that investment.

What we can do about it: Rather than spending public resources on an ineffective strategy to boost local employment (luring Amazon fulfillment centers), state and local governments should invest in public services (particularly in early-childhood education and infrastructure) that are proven to spur long-term economic development.

Update as of March 1, 2018: Since we ran our original analysis, additional data on fulfillment center openings has become available. We re-ran our analysis and found that the updated data confirm our previous results. See the Appendix for more information.

Introduction and key findings

Since its founding in 1994, Amazon’s network of fulfillment centers has grown to nearly 100 across the country. In 2017, publicly available data identified 95 Amazon fulfillment centers in 25 states. Current estimates suggest that fulfillment centers occupy over three-fourths of the total square footage of Amazon’s entire U.S. distribution infrastructure. (See Appendix Table 3 and methodology for data sources).

The expansion of Amazon’s physical distribution network has coincided with a strategic business plan of negotiating millions in tax abatements, credits, exemptions, and infrastructure assistance from state and local governments in the name of regional economic development. By the end of 2016, Amazon had likely received over $1 billion in state and local subsidies for its facilities, which would include not only fulfillment centers but “sortation” centers that only sort packages, mailing centers, and other facilities.1 In return for the incentives each of the fulfillment centers receives, Amazon claims to create hundreds of jobs with competitive pay and benefits.2

An analysis of these claims is timely. As Amazon looks to open a second headquarters in 2018, it is employing a similar strategy, on a much larger scale, exchanging tens of thousands of jobs for massive incentives in return. For example, the District of Columbia reportedly offered Amazon a permanent corporate tax rate cut as well as sales tax exemptions. According to The Washington Post, the announcement of the finalists in the running for hosting the new headquarters “also raised more difficult questions about the influence of large tech giants on cities and the possible unintended consequences of giving tax breaks and other benefits to an already successful corporate titan.”3

Using tax and other incentives to lure businesses to state and local areas is a long-running economic development strategy pursued by subnational governments. In nearly every state, businesses can receive a significantly lighter tax burden for constructing a sports stadium, filming a movie, or building a manufacturing assembly plant. The results on whether these types of community development strategies have a positive impact on job creation and growth is highly debated in popular news outlets and among researchers. And as Amazon has grown, the debate in some cases has specifically focused on Amazon.4

Studying the employment effects of opening Amazon fulfillment centers is an excellent opportunity to provide evidence for this debate. Using publicly available data on the opening of these fulfillment centers, we undertook a rigorous statistical assessment of claims that the opening of an Amazon fulfillment center in a specific county will provide broad employment gains to that local area.

Our key findings show that luring Amazon fulfillment centers is an ineffective strategy for boosting overall local employment

- The opening of an Amazon fulfillment center leads to an increase in warehousing and storage employment in the surrounding county. Two years after an Amazon fulfillment center opens in a county, warehousing employment in the county is approximately 30 percent greater. This effect is robust to numerous statistical controls.

- The opening of an Amazon fulfillment center does not lead to an increase in county-wide employment. Two years after an Amazon fulfillment center opens in a county, overall private-sector employment in the county has not increased. It is possible that the jobs created in the warehousing and storage sector are offset by job losses in other industries, or that the employment growth generated by Amazon is too small to meaningfully detect in the data. This finding of no effect is also robust to a series of statistical controls.

- The fact that some of our specifications show small reductions in county-wide employment—albeit not statistically robust—reinforces just how completely ineffective Amazon fulfillment center openings have been to providing any boost to overall local employment. The exact sign of the overall employment effect of opening an Amazon fulfillment center in a county is actually negative in some of our specifications, indicating that small reductions in county-wide employment follow these openings. Because this effect is not statistically robust across all statistical specifications, we do not claim reductions in county-wide employment but do assert that this effect supports the finding of no job growth.

State and local policymakers seeking maximum long-term benefits should reconsider extending tax incentives to lure businesses

The promise of luring jobs is nearly always and everywhere a very hard one for policymakers to ignore. The jobs gained by one locality that lures an establishment from another locality may be zero-sum, but they’re very visible and easy to point to. Jobs that are displaced by luring an establishment are more diffuse. And the specific jobs that could have been gained in the long-term by instead investing in education or other public goods are harder to celebrate—local officials can’t easily organize a ribbon-cutting ceremony around those kinds of jobs. Nevertheless, our findings support other research suggesting that state and local policymakers should consider the following points when debating whether to extend incentives to lure businesses:

Tax incentives likely constitute an unneeded giveaway

At an intuitive level, offering tax incentives for firms to move businesses to particular locales may strike some as sensible. All else being equal, firms likely would prefer to locate in a particular area if doing so lowered tax costs and hence increased profits. However, there are other considerations that significantly influence location decisions, including access to customers, the quality of public services needed to run businesses (for example, the existence of reliable electricity and high-quality roads) and access to a pool of qualified workers.5

Research has shown that state and local taxes are on average less than 2 percent of the cost of doing business. This means that simply offering to cut taxes won’t do that much to sway firms’ location decisions. In short these incentives are likely ineffective or, at best, an inefficient use of resources. These incentives are largely a windfall to firms that were going to locate in that spot even without the incentives, all while sacrificing revenue that areas need to invest in public goods.6

Tax incentives may do little to boost overall employment

While luring an establishment of an existing national employer to a specific state will create jobs at that establishment, it will not necessarily create more jobs overall. If, for example, labor supply in a particular locale is limited, job gains in the newly lured establishment could be offset by job losses among competitors. This is what happens when luring a Walmart into a county leads to shutdowns of local grocery stores—overall employment and economic activity is unaffected. Measuring the extent of this type of employment displacement is key to assessing the overall economic benefits of luring establishments of existing national chains. Our findings of the lack of overall job growth from opening an Amazon fulfillment center suggest that some sort of employment displacement is taking place, or that the growth in warehousing jobs is too limited to spill over into broad-based employment gains for the overall local economy. This is in keeping with a robust body of evidence indicating that reducing public services to provide tax cuts does not actually spur economic growth and job creation.7

Investments in public services are more effective than tax incentives at generating long-term economic growth

Another key downside of tax incentives is that they deprive states and localities of resources needed to invest in public goods, such as transportation or education. The research literature indicates that public spending and the expansion of public services increases local economic activity—and that such public investment is obviously hamstrung by policies (like offering tax incentives) that reduce resources available to state and local governments. Investments in public services (particularly in early-childhood education) and infrastructure are a much stronger recipe for spurring long-term economic development than providing tax increases to existing national employers.8

Amazon fulfillment centers

The expansive network of centers that store, pack, ship, and provide customer service for products is crucial to Amazon’s business model, which requires quick delivery throughout the country. As displayed in Figure A, construction of Amazon fulfillment centers in the United States increased significantly around 2008. Amazon had under 10 centers through the mid-2000s and had nearly one hundred by the end of 2017.9 The sharp rise in fulfillment centers corresponds with the 2005 introduction of Amazon Prime, in which subscribers pay an annual fee for two-day shipping and other benefits, and the 2006 launch of Fulfillment by Amazon, in which participating sellers have their items stored, packed, and shipped by Amazon.

FIGURE A

Total number of Amazon fulfillment centersCumulative openings, 1997—2017

| Date | Cumulative openings |

| 1997q4 | 1 |

| 1998q1 | 1 |

| 1998q2 | 1 |

| 1998q3 | 1 |

| 1998q4 | 1 |

| 1999q1 | 1 |

| 1999q2 | 2 |

| 1999q3 | 2 |

| 1999q4 | 2 |

| 2000q1 | 2 |

| 2000q2 | 2 |

| 2000q3 | 2 |

| 2000q4 | 3 |

| 2001q1 | 3 |

| 2001q2 | 3 |

| 2001q3 | 3 |

| 2001q4 | 3 |

| 2002q1 | 3 |

| 2002q2 | 3 |

| 2002q3 | 3 |

| 2002q4 | 3 |

| 2003q1 | 3 |

| 2003q2 | 3 |

| 2003q3 | 3 |

| 2003q4 | 3 |

| 2004q1 | 3 |

| 2004q2 | 3 |

| 2004q3 | 3 |

| 2004q4 | 3 |

| 2005q1 | 3 |

| 2005q2 | 4 |

| 2005q3 | 6 |

| 2005q4 | 7 |

| 2006q1 | 7 |

| 2006q2 | 8 |

| 2006q3 | 8 |

| 2006q4 | 8 |

| 2007q1 | 8 |

| 2007q2 | 8 |

| 2007q3 | 11 |

| 2007q4 | 11 |

| 2008q1 | 11 |

| 2008q2 | 12 |

| 2008q3 | 14 |

| 2008q4 | 16 |

| 2009q1 | 16 |

| 2009q2 | 16 |